Quarterly Letter

“I am all for Artificial Intelligence (AI). There is a shortage of the real thing.” – Charlie Munger

There is a lot to question in today’s world, but one thing is clear – the U.S. economy continues to display remarkable resilience. Corporate earnings maintain their steady climb, the labor market exceeds expectations, consumer spending is strong and the inflation picture, while elevated, will likely improve given lower energy costs over the balance of the year. As a result, the stock market, which is currently trading at twenty-one times projected earnings, is not unreasonably valued, particularly when compared to its earnings growth potential.

Corporate earnings are largely driven by innovation and productivity growth – they are the DNA of our economic system. Given that, when you combine the genius of our tech entrepreneurs with capital markets having access to tons of money, profit margins expand. When that occurs, the result is often what happened in this past quarter – stock prices rising. It is a marvel to behold.

One might think that given another six months of positive outcomes stock price valuations would be overly stretched. Well, to be fair, the market is on the high side. Yet, at current levels, it is actually trading at a lower valuation than where it began the year, despite many stocks being up double digits since January. More surprisingly, the stock market is now trading at a valuation similar to where it stood six years ago, in the early days of COVID.

That said, stock market gains have been uneven, and for every semiconductor stock that has doubled or quadrupled, there are financial or consumer discretionary companies where stock prices have hardly moved. Indeed, corporate earnings growth has been heavily dependent on AI and infrastructure spending, primarily on data centers along with those companies which build and supply them. That fact is worrisome, as a concentration of profit gains among a select few companies does increase short-term downside risk for the market. In addition, the gargantuan “spend” that the hyper-scalers (such as Alphabet, Amazon, Meta and Microsoft) are willing to invest in data centers will likely negatively impact their earnings for years to come. For the investor, the debate is whether this massive spend will prove smart over time. Most pundits believe it will, but there is no question that some companies will fare much better than others.

In other news, the IPO (Initial Public Offering) market has seen new life in 2026, and this past quarter witnessed the debut of SpaceX as a publicly traded company. It was the largest IPO in history. SpaceX is an amazing story, and investing in Elon Musk companies over the years has almost always been a successful strategy, albeit one light on current earnings to justify their success. That is particularly true for SpaceX, sporting a multi-trillion valuation, but no real earnings . . . yet.

Likewise, we will have Anthropic and OpenAI also go public in upcoming months. Their AI models are literally changing the world, more so each week and month. Through their large language models (Claude and ChatGPT, respectively) they produce tens of billions of dollars in revenues, have software already used by millions, have major enterprise partnerships in place and are well-funded. However, neither has sustained profits . . . yet. That is the key. How long will it be before sustainable, growing profits can be realized? After some base level of expense, digital products like theirs are replicated with minimal incremental costs. Thus, profits should climb, perhaps by the bucket-load. We like all three of these companies, particularly SpaceX and Anthropic, but finding an attractive price to pay for initial purchases is difficult, especially in a momentum market such as we have. It is always dangerous to rush to make an investment when many buyers of stocks seem willing to pay almost any price.

Mark Cuban recently said, “Learn AI or become a dinosaur within three years.” We tend to agree. The surge in AI investment can be expected to make companies smarter, more efficient and much more productive. History suggests companies that are early in adopting productivity-enhancing technologies are often able to maintain profit growth well into the future. It is a lesson many companies seem to have learned, and that bodes well for future stock market gains. Nonetheless, be prepared for some turbulence. We believe the second half of 2026 will see strong corporate earnings, but stock returns seem unlikely to be as rewarding as in the first half. We still have a war or two to settle and midterm elections rarely instill short-term confidence in investors. Even so, we do not manage money for the next quarter or two – we manage for the fundamentals longer-term. We remain confident in the course ahead.

Market Commentary

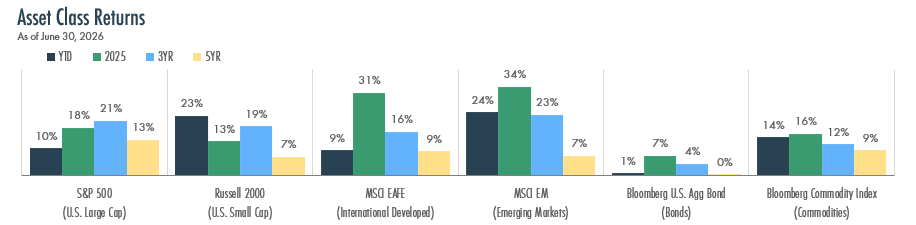

Markets staged a strong rebound in the second quarter, recovering the ground lost during the first quarter’s selloff and closing the first half of the year higher across nearly every major asset class.

- U.S. Large Cap stocks, as measured by the S&P 500, are now up 10% year-to-date, bolstered by resilient corporate earnings and with semiconductor stocks leading the charge.

- U.S. Small Cap stocks, as measured by the Russell 2000, have performed even better, up 23% for the year – a healthy sign the rally is broadening beyond the largest technology companies.

- International stocks also participated. Developed Markets have gained 9% year-to-date, while Emerging Markets have surged 24%.

- Bonds are up 1% for the year, as income from higher yields has been offset by the market price drag from a modest rise in interest rates.

- Commodities are up 14% year-to-date, but it has been a wild ride. Oil prices, which spiked earlier this year following the conflict in Iran, gave back much of those gains during the quarter amid a temporary ceasefire. Gold surged early also only to end the half down from the start of the year.

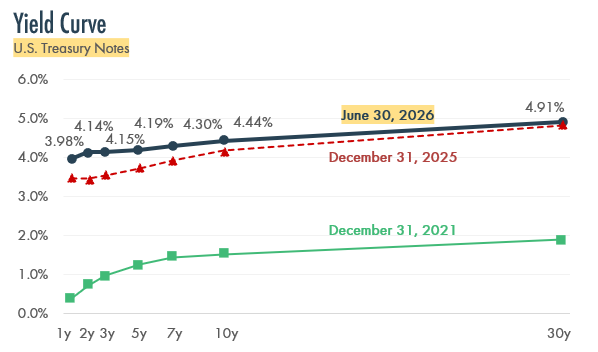

Kevin Warsh took over as Fed Chair in May and presided over his first policy meeting in June, where the Fed held short-term interest rates steady at 3.50% – 3.75%. With inflation still running well-above the Fed’s 2% target, some believe that the next move could be an interest rate increase rather than a cut.

A New Regime at the Fed

A changing of the guard occurred at the Federal Reserve in May. Kevin Warsh succeeded Jerome Powell as Fed Chair and led his first policy meeting in June, where the committee voted unanimously to hold interest rates steady.

Warsh has wasted little time putting his stamp on the institution. The Fed’s June policy statement was roughly a third the length of the prior one, reflecting Warsh’s preference for saying less about where interest rates are headed. He has emphasized the Fed’s determination to bring inflation back down to target.

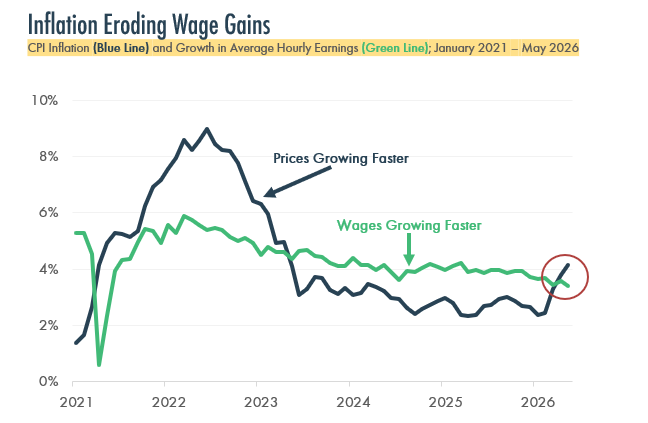

Inflation has climbed to just over 4% – its highest level in roughly three years and more than double the Fed’s 2% target. Driven largely by this spring’s energy price shock, consumer prices are once again rising faster than the average worker’s paycheck, eroding purchasing power, as seen below.

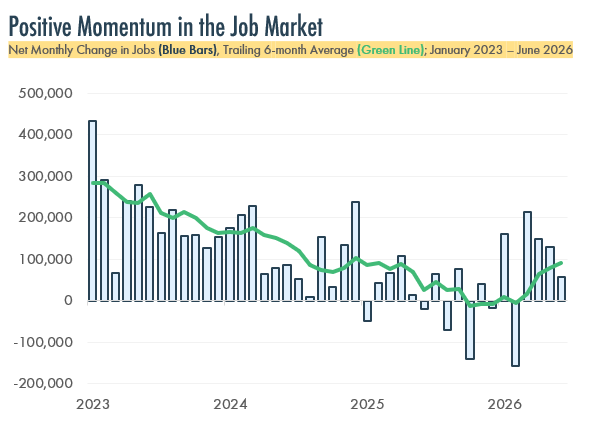

The job market has given the Fed room to stay patient for now. As shown in the bottom right, monthly job growth has regained momentum in 2026 after a soft stretch last year.

Earnings Are Doing the Heavy Lifting

Source: Bloomberg

Despite elevated inflation and a Fed signaling that rate cuts are off the table for now, stocks reached record highs in the second quarter, largely due to very healthy corporate profits.

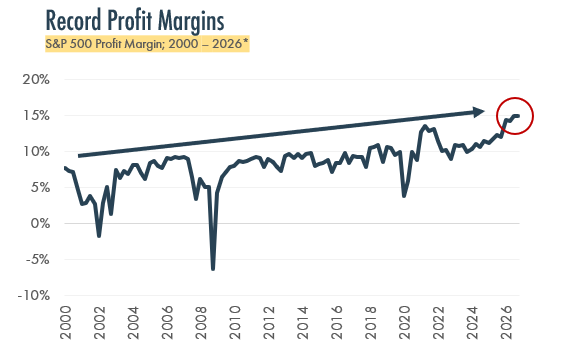

Companies in the S&P 500 are not just earning more, they are keeping more of every dollar of sales. As shown to the right, profit margins have climbed for more than two decades and now sit near record levels. Productivity gains resulting from technology enhancements seem the likely driver for this.

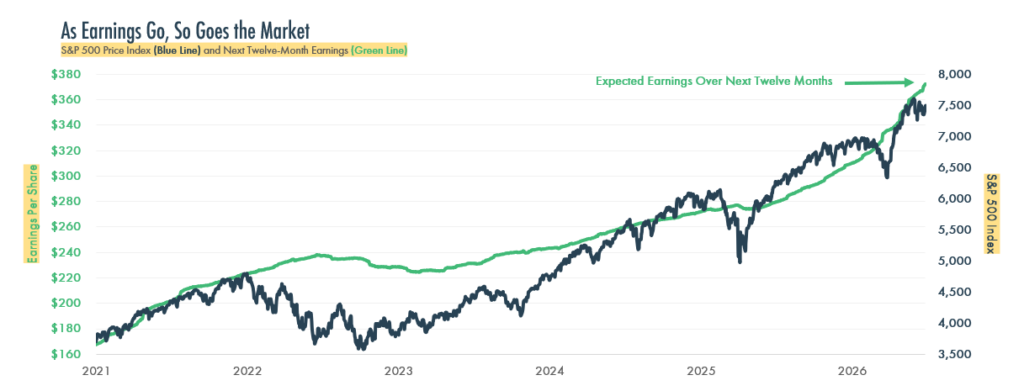

Ultimately, earnings growth drives stock prices over the long-term. As seen below, the S&P 500 Index has tracked the earnings that its companies are expected to generate over the coming year. Prices and earnings drift apart at times, but rising profits have always been the engine behind long-term stock market gains.

AI Angst Broadens Market Leadership

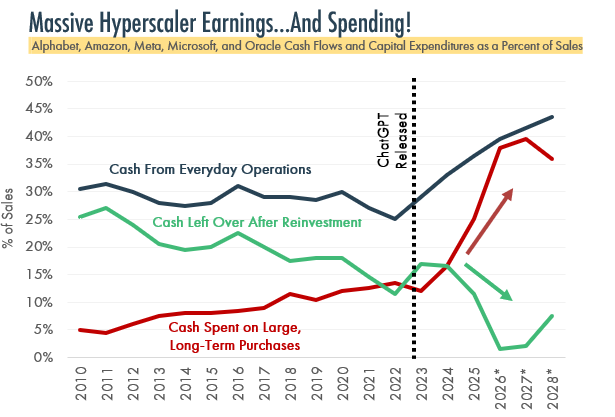

The world’s largest technology companies are generating enormous amounts of cash — and spending nearly all of it. As shown to the right, the cash these companies produce from everyday operations has never been higher as a share of sales. But spending on data centers, semiconductor chips, and other long-term AI investments has grown even faster, leaving less cash left over than at any point in more than a decade. Estimates suggest that gap begins to close by 2028, but those projections depend on current and planned AI investments paying off.

Investors have taken notice. The Magnificent 7 — the mega-cap technology stocks that powered the market for much of the past three years — have declined 2% this year, even as the broader market has climbed. Investors are questioning whether the future return on investment will be justified by the massive expenditures of today.

Market leadership changes — and sometimes quickly. The stocks that dominate one period are rarely the leaders of the next, making a strong case for remaining diversified.

Source: Bloomberg

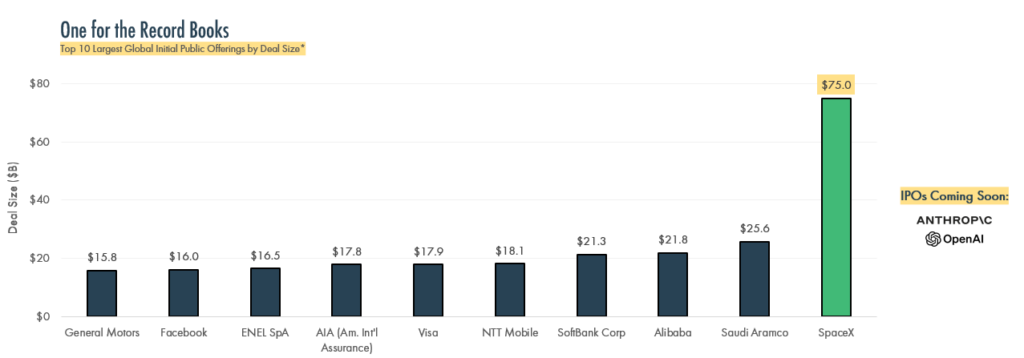

SpaceX: A Record-Setting Initial Public Offering

After years of anticipation, SpaceX went public in June in the largest initial public offering (IPO) in history, raising roughly $75 billion — nearly three times the previous record set by Saudi Aramco in 2019, as shown below.

That IPO record may not last long, as OpenAI and Anthropic – two of the largest artificial intelligence companies – each filed paperwork to go public, likely sometime later this year.

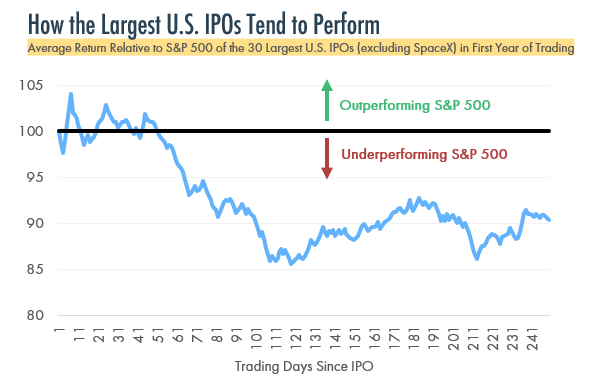

Excitement, however, is not the same as investment merit. As shown to the right, the 30 largest U.S. IPOs have, on average, trailed the S&P 500 over their first year of trading. Companies attracting the most attention at their debut have often seen much of their early growth prior to the IPO, i.e., before retail investors get access. That does not mean these companies will fail, but it is a reminder that discipline and diversification matter most when enthusiasm runs highest.

Contributors

@ 2026 The Finerty Team

The S&P 500 Index is a free-float capitalization-weighted index of the prices of approximately 500 large-cap common stocks actively traded in the United States. The Bloomberg US Aggregate Bond Index is a broad base, market capitalization-weighted bond market index representing intermediate term investment grade bonds traded in the United States. The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment advisor does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified. Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.

© 2026 Steven L. Finerty, J.D., CFP®, Logan W. Finerty, CFA, CFP®, Jeffrey T. Wist, J.D., CFP®, Susan E. Brown, CFP®, Timothy C. Burford, CFA, Jerrod C. Anderson, CFA, CFP®. Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment adviser does not imply a certain level of skill or training.