Quarterly Letter

“To swim a fast 100 meters, it’s better to swim with the tide than to work on your stroke.” – Warren Buffet

After a rocky start to the year given concerns over tariffs, inflation and large federal deficits, the global stock market has staged a strong rebound—with the third quarter of 2025 marking its best performance in more than a decade. Leading the charge have been companies with an artificial intelligence (AI) story; producing a surge of noteworthy price gains driven by remarkable innovation paired with underlying strength in both revenues and earnings. Companies without an AI narrative have had more tepid gains, frustrating many active stock managers who have been challenged to keep up. Bottom line: swimming with the AI tide in 2025 has not just been a component of performance, it has been a prerequisite. We are reminded of the great investor, Jeremy Grantham’s comment, “Ninety percent of what passes for brilliance or incompetence in investing is the ebb and flow of investment style.” Overwhelmingly, AI is the current investment style du jour.

According to JP Morgan research, AI stocks have accounted for seventy-five percent of S&P 500 Index returns since November 2022, when ChatGPT launched. Even more amazing, AI stocks have represented eighty percent of the earnings growth in the S&P 500 Index over that time period, and ninety percent of capital spending has been related to AI. AI is so transformative that data center construction nationwide is now outpacing office construction. AI is also having a huge impact on the power grid – AI has a monstrous appetite for power, and natural gas and nuclear plants take years if not decades to build.

All that said amidst this AI euphoria, we remind ourselves of what Bill Gates said about technology, “We always over-estimate the change that will occur over the next two years and underestimate the change that will occur in the next ten.”

Given the overall run in the stock market – and it is not just a U.S. story, as foreign stocks have done even better this year – it is logical to expect some moderation in returns near term, or even one of those unpleasant corrections that occur with regularity. To that point, valuations are on the high side, tariff uncertainty persists, and wars continue overseas. Closer to home, housing, trucking, and our labor markets are softer than desired, and mortgage rates remain higher than desired while budget deficits continue on their unsustainable long-term path. Clearly, there is a plethora of legitimate reasons to be concerned.

Yet amidst all this, we still feel optimistic, and remind ourselves that nervous energy – the temptation to sell – has historically been the great destroyer of wealth for long-term investors. As we see things, the U.S. economy is still fairly healthy. Goldilocks might note that it is not too hot, but also not too cold. On the positive side, we had one interest rate cut by the Fed in September, and two more seem likely this year; perhaps more next year. Tariffs this year have had an impact, but to-date have not had the negative impact on inflation many feared. Even the weak dollar this year is not all bad news. Multinational firms can turn overseas profits into higher earnings when they convert their foreign earnings back to dollar denomination. Thus, talk of a recession, which many have been predicting since 2022, seems premature against this backdrop.

More to the point, if there is one behavioral truth we have learned, it is that the stock market performance can never be consistently forecasted. Therefore, to enjoy the eminently predictable long-term advance of a stock portfolio, the only logical choice is to always be in the market. Sure, tweaking of portfolios is always prudent, and shifts in sector weightings between technology utilities, consumer staples, industrials, energy, etc. is also appropriate. But the long-term tide has always gone up. We will continue to swim with it.

“We always over-estimate the change that will occur over the next two years and underestimate the change that will occur in the next ten.” – Bill Gates

Market Commentary

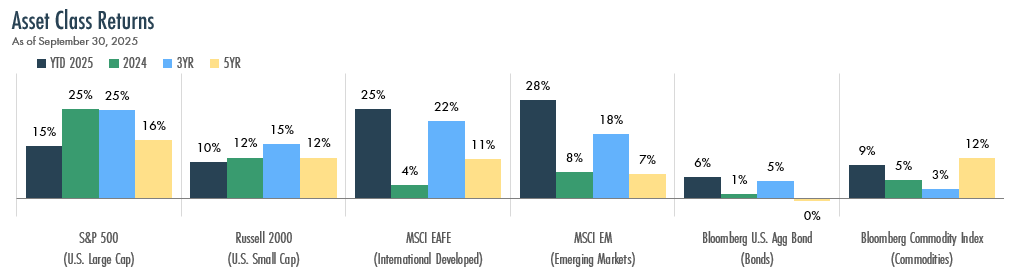

- Nearly all major asset classes posted positive returns in the third quarter, continuing the sharp recovery off April’s lows.

- U.S. Large Cap stocks, as measured by the S&P 500 Index, registered their fifth straight month of gains in September, and are now up 15% year-to-date. U.S. Small Cap stocks had a strong quarter, gaining 12% and moving Small Caps into positive territory for the year.

- International stocks continued to build on their remarkable year. Developed and Emerging Markets are up 25% and 28%, respectively, benefitting from a weaker U.S. dollar and more accommodative monetary policy abroad.

- Bonds, as measured by the Bloomberg U.S. Aggregate Bond Index, are up 6% year-to-date, putting them on pace for their best year since 2020.

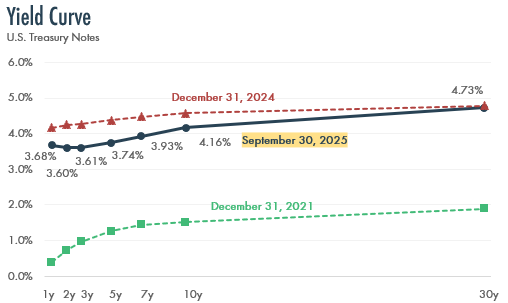

- In September, the Federal Reserve cut short-term interest rates by 0.25% to 4% after pausing earlier in the year due to tariff-driven inflation concerns. Chairman Powell characterized the most recent cut as a precaution to support the labor market while still supportive of maintaining downward pressure on inflation. Job growth, while still positive, has slowed in recent months.

Climbing a Wall of Worry

Since bottoming in March, 2009 amid the Great Financial Crisis, the S&P 500 Index has delivered an extraordinary 1,241% return including dividends despite a long list of crises, including trade wars, a global pandemic, the highest inflation in 40 years, aggressive Fed rate hikes, a major European war and U.S. government shutdowns.

The market’s resilience underscores a critical lesson for investors: short-term volatility caused by the latest headlines, while unsettling, has been a poor reason to abandon a long-term strategy. Staying invested through periods of uncertainty has proven immensely rewarding for patient investors.

- The Federal Reserve reduced short-term interest rates for the first time this year in September, lowering the federal funds target rate by 0.25% to a range of 4.00% – 4.25%. Fed officials cited a softening labor market as a more pressing concern than inflation, which remains above the Fed’s long-term target.

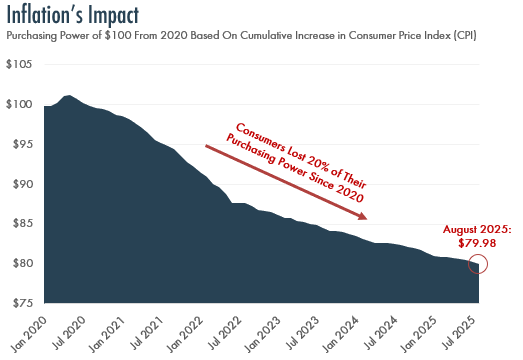

- Although the rate of inflation has come down substantially from its peak in 2022, its cumulative impact on consumers’ budgets cannot be overstated. As shown below, consumers have lost 20% of their purchasing power since 2020, highlighting the importance of investing for growth over the long-term.

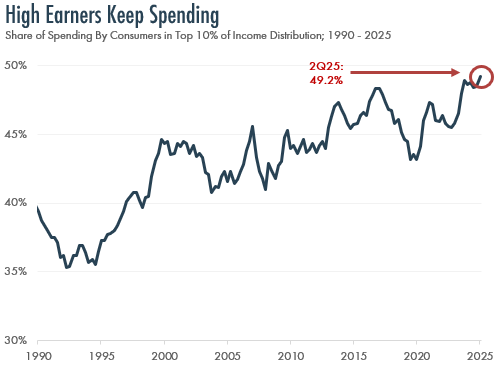

- Inflation’s effects are particularly challenging for those on fixed incomes or whose wages have not kept pace with price increases. As these consumers hold back on some purchases, the highest earners have grown to account for nearly half of all consumer spending, as shown in the bottom right.

Meme Stocks Return

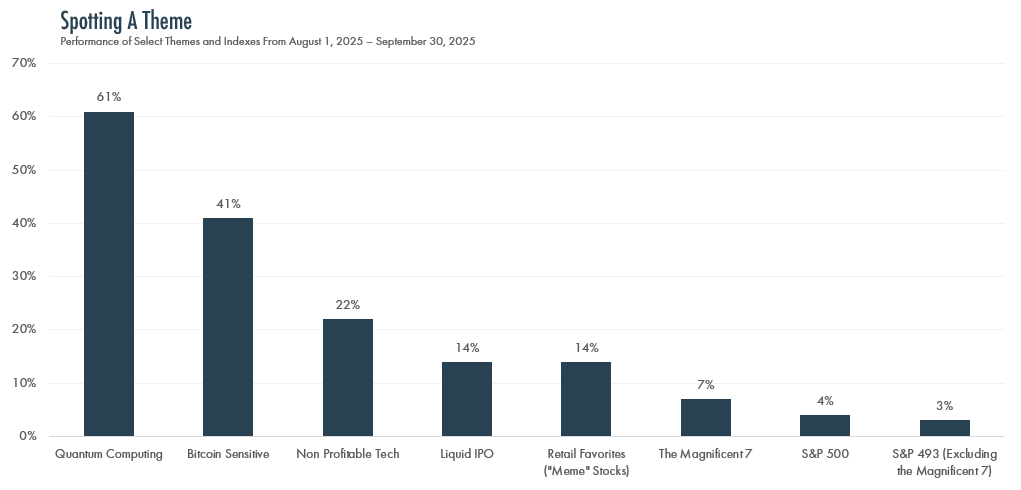

While the market’s recovery from April’s lows has been welcomed by investors, the rally has more recently been driven by speculative, thematic and what are sometimes referred to as “meme” stocks, or those in vogue, or a fad.

As shown below, momentum-driven themes and companies with a connection to the AI narrative handily outpaced a broad, quality index such as the S&P 500, creating a challenging environment for investors focused on a business’s fundamentals. In layman’s terms, if an investor was not heavily invested in companies which might benefit from quantum computing, the genesis of artificial intelligence (AI), in block-chain technology (think Bitcoin and stable coins) or in companies not profitable today, but potentially very profitable in the future, returns were much more modest.

Over time, there is nearly always a reversion to the mean. Given that, it is reasonable to expect quality-oriented companies to perform relatively better going forward. Companies with strong cash flows, growing top and bottom lines and pristine balance sheets have historically done extremely well.

It is an AI Buildout Mania

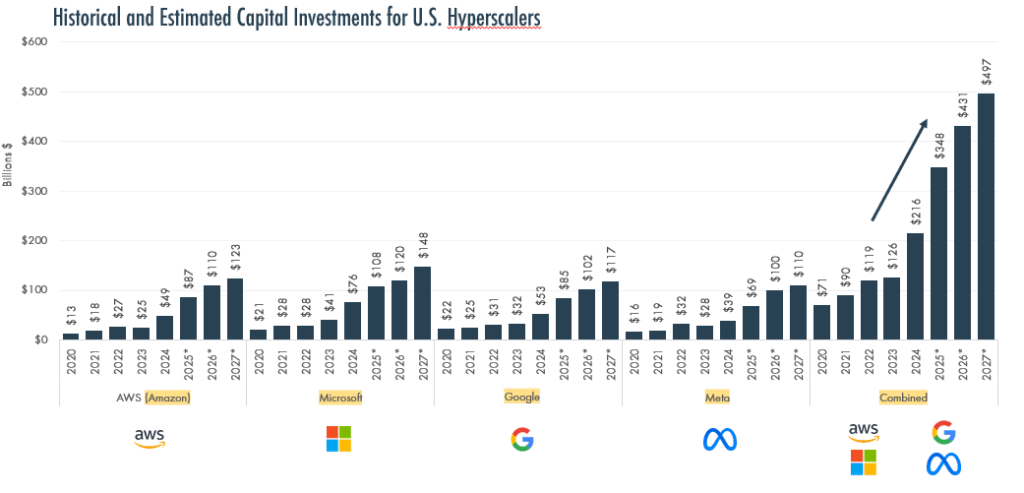

Technology companies have committed to spending an extraordinary amount of money to build the infrastructure required to train and run advanced AI models, a trend that is expected to continue for many years. As shown below, the four largest U.S. hyperscalers – or companies, such as Microsoft, that provide scalable computing power and data storage – are expected to spend nearly $500 billion in 2027 alone – an amount roughly equal to Norway’s entire economic output.

One company’s spending is another company’s income. Thus, this unprecedented buildout has benefited multiple sectors beyond Technology, from real estate developers specializing in data centers to power generation companies. The AI infrastructure boom represents one of the largest coordinated capital spending cycles since the Dot.com era, and much of this investment is occurring within the U.S.

AI has a monstrous appetite for power, and the increased electricity demand will require a large number of new and refurbished natural gas and nuclear plants to provide it. It will take years, if not decades, to meet expected demand, and will also be a factor in future electric rates for consumers.

Source: Goldman Sachs Global Investment Research

Contributors

© 2025 The Finerty Team

The S&P 500 Index is a free-float capitalization-weighted index of the prices of approximately 500 large-cap common stocks actively traded in the United States. The Bloomberg US Aggregate Bond Index is a broad base, market capitalization-weighted bond market index representing intermediate term investment grade bonds traded in the United States. The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment advisor does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.